EU autumn economic forecast for Bulgaria: Subdued growth amid rising uncertainty

The European Union’s autumn economic forecast for Bulgaria, released on November 4, sees real GDP growth in the country as expected to remain muted, deflation turning to inflation by 2016 and the general government deficit remaining above three per cent over the forecast horizon.

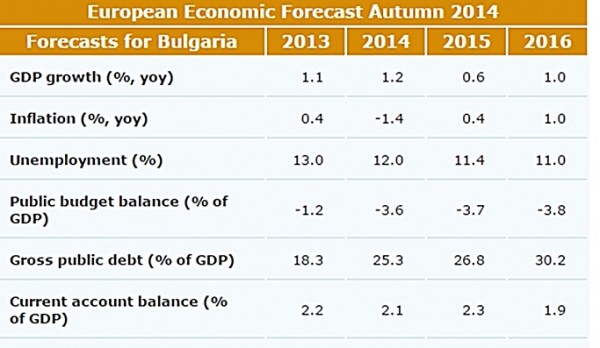

“Real GDP growth is expected to remain muted, falling from 1.2% in 2014 to 0.6% in 2015 and 1% in 2016 as domestic demand weakens,” according to the EU autumn economic forecast.

“After a deflationary period in 2014, inflation is set to only slowly pick up to one per cent by 2016. Following a sizeable fiscal deterioration in 2014, the general government deficit is projected to remain above three per cent of GDP over the forecast horizon.”

Downside risks have materialised since the spring forecast, the EU said.

A less dynamic external environment was weighing on exports.

In June, confidence in the domestic segment of the banking sector received a setback, when a bank run led to the fourth largest bank (this is a reference to Corporate Commercial Bank) closing leaving no access to deposits for at least five months.

Irregularities in banking practices have also surfaced, the report said.

“This forecast assumes an orderly unfolding of the banking situation, with domestic banks considerably tightening credit standards, thereby depressing investment by firms.”

Survey indicators already indicate a significant deceleration of activity over the rest of 2014,

leading to an average GDP growth rate of 1.2 per cent for the year as a whole. These headwinds are expected to continue, resulting in real GDP growth of 0.6 per cent in 2015 and one per cent in 2016.

Private consumption was supported in the first half of 2014 by the sharp increase in households’ real disposable income driven by high dynamics of public sector wages and pensions as well as deflation, the report said.

“Recent monthly consumer confidence and retail data, however, suggest that private consumption will lose momentum by 2015.”

Similarly, gross fixed capital formation is mainly driven by buoyant government investment

spending on the back of accelerated absorption of EU funds in 2014, the forecast said.

“However, as the current programming period is coming to an end, EU funded investment is set to decline significantly in the coming years.”

In turn, private investment is seen to contract further in 2014-15, mirroring the on-going deleveraging process in the economy and low profit expectations amid increased uncertainty.

Overall, investment is projected to decline in both 2015 and 2016, the EU autumn economic forecast said.

Despite a slowdown in the first half of 2014, exports are set to resume growing at a moderate pace in 2015-16, sustained by the mild recovery in both the EU and non-EU trade partners.

On the back of a further slowdown in domestic demand, the contribution of net trade to overall economic growth is projected to turn positive in 2015, while the current-account surplus is seen stable at about two per cent of GDP by 2016.

Manufacturing and construction continued to shed labour, but the overall labour market outcome in 2014 is supported by temporary employment in the volatile agricultural sector, the report said.

Slow economic growth is set to result in small declines in employment over 2014-15, followed by only modest gains in 2016.

Nevertheless, combined with a continued decline in the labour force due to negative demographic trends, this brings the unemployment rate from a peak of 13 per cent in 2013 to 11 per cent by 2016, the forecast said.

Risks still appear tilted to the downside, according to the forecast.

“On the domestic front, accelerating confidence deterioration in the banking sector and a more protracted period of disruptions to credit intermediation alongside tighter credit conditions pose considerable risks.”

“A more prolonged weakness of business and consumer confidence together with the still fragile labour market could lead to a reduction of domestic demand further eroding confidence in the economy.”

On the external front, the country’s dependence on Russian gas imports could become a further burden to growth should supplies be disrupted, the forecast said.

Bulgaria has been experiencing deflation since mid-2013, and prices this year are expected to decline by an average -1.4 per cent.

This has been caused by a coincidence of falling global energy prices, significant administrative cuts to electricity and health care prices, and declining food prices due to

a good harvest.

Also, core inflation has turned strongly negative, reflecting overall weak domestic

demand. Some of these deflationary factors are temporary in nature and their base effects will fade over the second half of 2014.

Moreover, the Bulgarian government has decided to increase electricity prices by 10 per cent as of October 2014 and tobacco excise will be hiked in 2015.

Aggregate HICP is forecast to pick up only modestly in 2015, to 0.4 per cent, and one per cent in 2016.

The general government deficit is projected to deteriorate from 1.2 per cent in 2013 to 3.6 per cent of GDP in 2014.

This is significantly more than planned in the original 2014 budget, the forecast noted.

This projection includes the 2014 budget update proposal of the caretaker government made in September, which also reveals a significant expenditure increase, according to the forecast.

Also, VAT, excises and some non-tax revenues have underperformed over 2014.

“Under a no-policychange assumption, the general government deficit is set to weaken further to 3.7 per cent of GDP in 2015 and to 3.8 per cent in 2016, in line with the projected

sluggish evolution in tax bases.”

The forecast did not include assumptions about measures in the upcoming 2015 budget.

“In structural terms, the deficit is estimated to deteriorate by over 2 pps. of GDP in 2014 and to stay broadly flat in 2015-16.

“The general government gross debt is forecast to increase rapidly from 18.3 per cent of GDP in 2013 to about 25 per cent in 2014, reflecting not only the financing of the current year’s fiscal deficit, but also the roll-over of a large bond maturing in January 2015 and the existing liquidity scheme for the stabilisation of the financial sector.”

The forecast did not include any potential further debt issuances to support the financial sector.

The debt ratio is forecast to amount to slightly above 30 per cent of GDP in 2016.